Companies must amend business practices to comply with new governmental mandates and market-based incentives aimed to meet the International Panel on Climate Change (IPCC) goal of 85 percent carbon dioxide emission reduction by 2050¹ . Addressing greenhouse gas (GHG) emissions can identify opportunities to bolster the bottom line, reduce risk, and discover competitive advantages.

The GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard ² responds to the demand for an internationally accepted method to enable GHG company value chain management. To better support organisations’ compliance, the GHG protocol has produced the following separate, but complimentary, standards:

GHG Protocol Corporate Accounting and Reporting Standard (2004): A standardised methodology for companies to quantify and report their corporate GHG emissions. Also referred to as the Corporate Standard.

GHG Protocol Product Life Cycle Accounting and Reporting Standard (2011): A standardised methodology to quantify and report GHG emissions associated with individual products throughout their life cycle. Also referred to as the Product Standard.

GHG Protocol for Project Accounting (2005): A guide for quantifying reductions from GHG-mitigation projects. Also referred to as the Project Protocol.

GHG Protocol for the U.S. Public Sector (2010): A step-by-step approach to measuring and reporting emissions from public sector organisations, complementary to the Corporate Standard.

GHG Protocol Guidelines for Quantifying GHG Reductions from Grid-Connected Electricity Projects (2007): A guide for quantifying reductions in emissions that either generate or reduce the consumption of electricity transmitted over power grids, to be used in conjunction with the Project Protocol.

GHG Protocol Land Use, Land-Use Change, and Forestry Guidance for GHG Project Accounting (2006): A guide to quantify and report reductions from land use, land-use change, and forestry, to be used in conjunction with the Project Protocol.

Measuring to Manage: A Guide to Designing GHG Accounting and Reporting Programs (2007): A guide for program developers on designing and implementing effective GHG programs based on accepted standards and methodologies

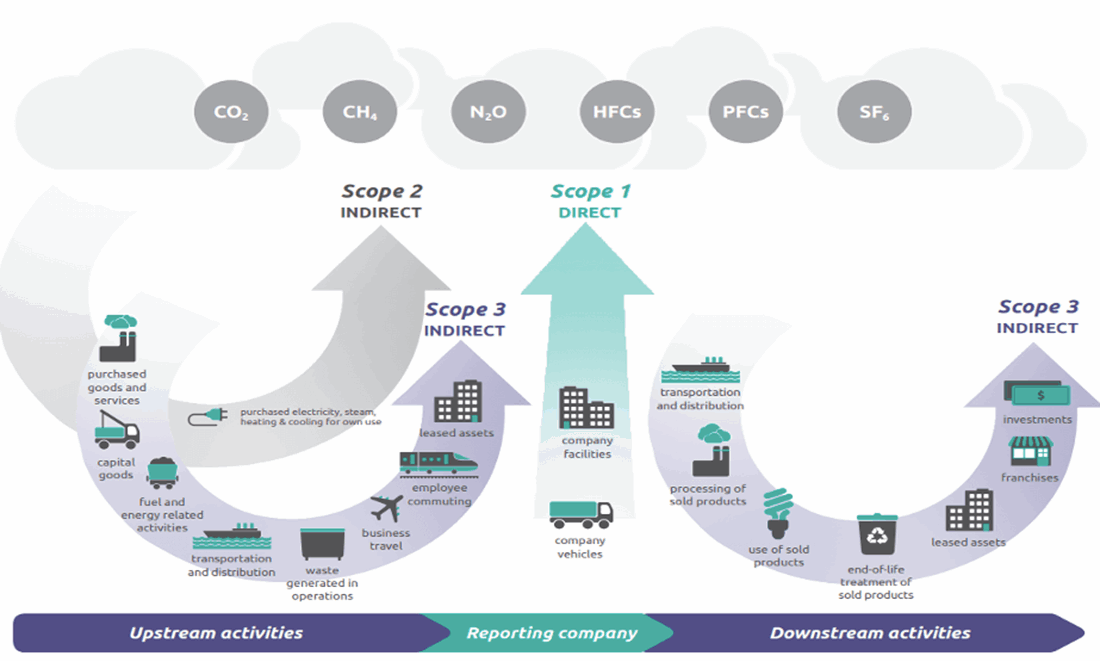

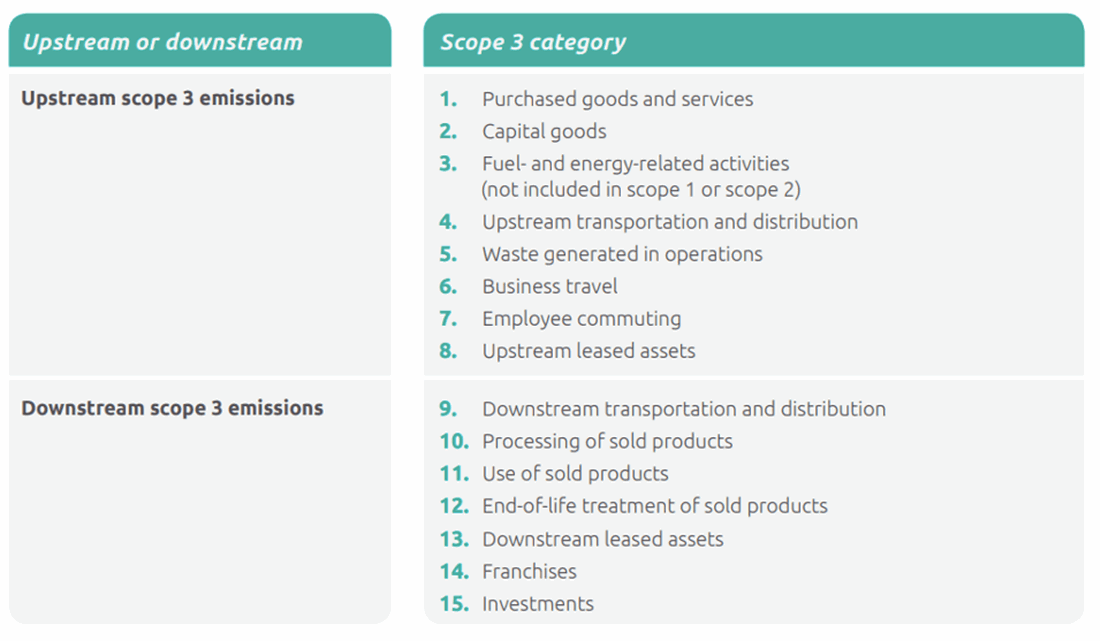

The following is an overview of the GHG emissions from scopes 1, 2 and 3 across each stage.

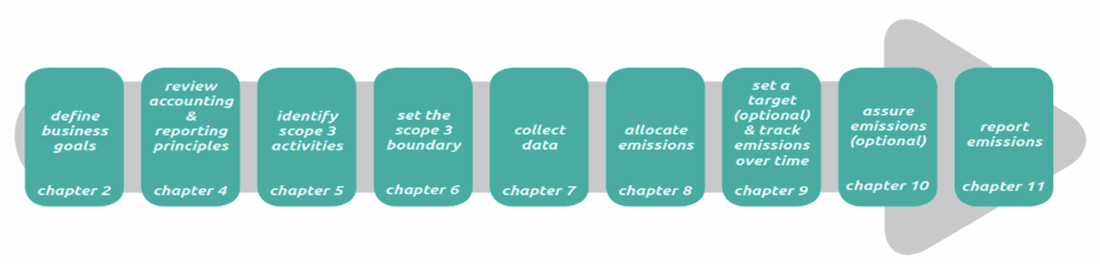

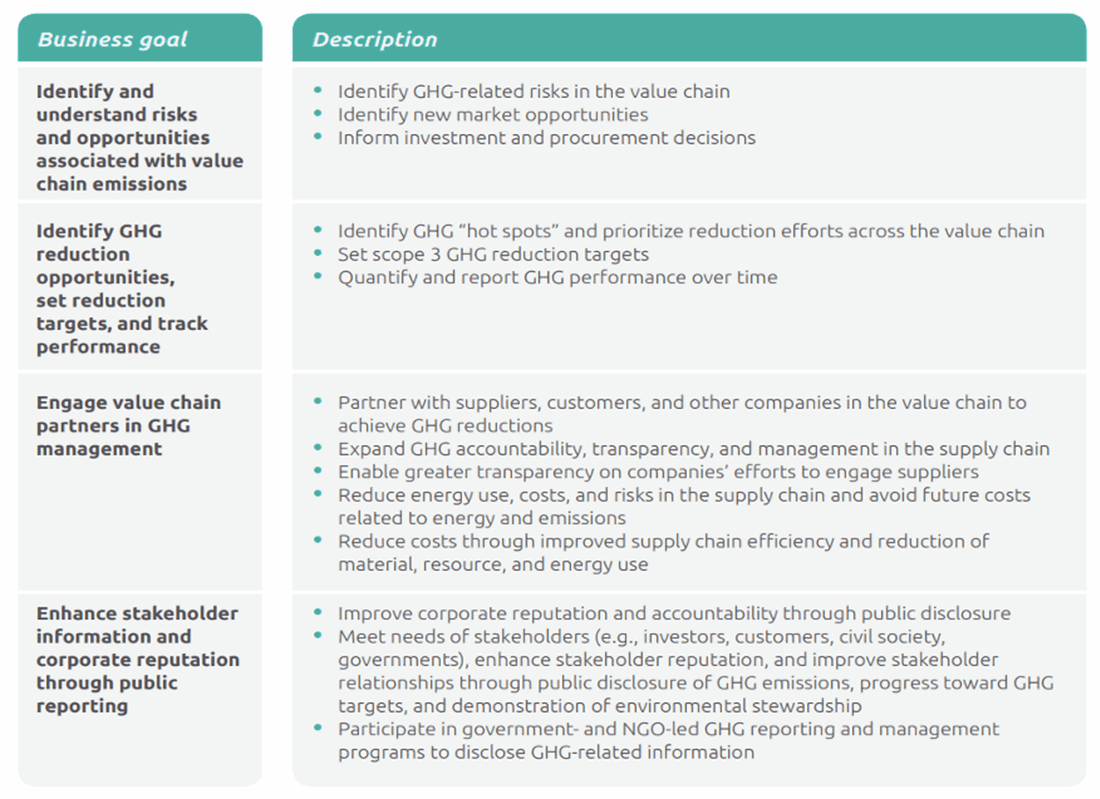

Before accounting for scope 3 emissions, companies should consider which business goal(s) are highest priority. The GHG protocol has produced a simple table to illustrate the most common scenarios business attribute to their development of scope 3 inventory.

Legislative Position

United States

In March 2022, the SEC proposed amendments to its rules under the Securities Act of 1933 and the Securities Exchange Act of 1934 that would require SEC registrants to provide certain climate-related information in their registration statements and annual reports. The proposal would require SEC registrants, including foreign private issuers, to include certain climate-related disclosures in their registration statements and periodic reports, including annual reports on Form 10-K and, in the case of foreign private issuers, Form 20-F.

At the time of compiling this research the timetable is as follows:

- March 21, 2022: SEC released new proposals for climate-related risk disclosures.

- June 17, 2022: End of the comment period for the new proposals.

- February 2024: First disclosures on Scope 1 and 2 for large organisations.

- February 2025: Disclosures on Scope 3 emissions and emissions intensity required for large organisations

International

On 21st October the ISSB voted unanimously to require companies to disclose Scope 1, 2 and 3 greenhouse gas emissions, to include that of indirect emissions related to the goods or services a reporting company uses throughout the supply chain.

The ISSB also announced that it would develop relief provisions to help companies apply the Scope 3 requirements, including giving more time for reporting companies’ disclosures and developing “safe harbour” provisions. Refining the International Financial Reporting Standards (IFRS) S1 (general sustainability-related financial information disclosure) and S2 (climate-related disclosures) are the initial focus. Further rules are projected to be released in early 2023.

United Kingdom

The rules about Scope 3 are part of the UK government’s Streamlined Energy and Carbon Reporting (SECR) policy.

Fuel burned during business travel of employee-rented or owned vehicles on behalf of large unquoted companies and large LLPs is the only Scope 3 emission reporting currently required. This means applicable organisations must document the vehicles’ energy consumption and use a conversion guide to calculate resulting emissions. Quoted companies (those listed in the stock exchange) are not required to report, though strongly encouraged.

European Union

There is no current Scope 3 reporting legislation, though that is likely to change under the Non-Financial Reporting Directive 2014/95/EU, and will likely target vehicle impacts first. The EU attributes its lack of requirements to GHG protocols not sufficiently addressing the holistic reporting structure needed to accurately evaluate a company’s impact.

Principles

Relevance: Ensure the GHG inventory appropriately reflects the GHG emissions of the company and serves the decision-making needs of both internal and external users.

Completeness: Account for and report on all relevant GHG emission sources Disclose and justify any specific exclusions.

Consistency: Use consistent methodologies to allow for meaningful performance tracking of emissions over time. Transparently document any changes to the data, inventory boundary, methods, or other relevant factors in the time series.

Transparency: Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used.

Accuracy: Ensure that the quantification of GHG emissions is as accurate as possible, with little uncertainty. The integrity of the data enables confident decision making.

Approach: Most organisations will likely prioritise the materiality of their emissions to make a meaningful start at implementing the new requirements and will learn as they go. An ideal approach to initiating the reporting procedures is to segment the supply chain into upstream and downstream categories.

In terms of data that is needed the approach should consider:

- Prioritisation by impact or opportunity

- Spend and/or revenue

- Volume consumed

- Influence over activities

- Risk and/or risk exposure

- Primary data followed by secondary data (industry benchmarks)

- Data accuracy

- Expanding beyond tier 1 suppliers – timeframe and resources needed

- Use of proxy data to fill “data gaps”

Considerations and Commentary

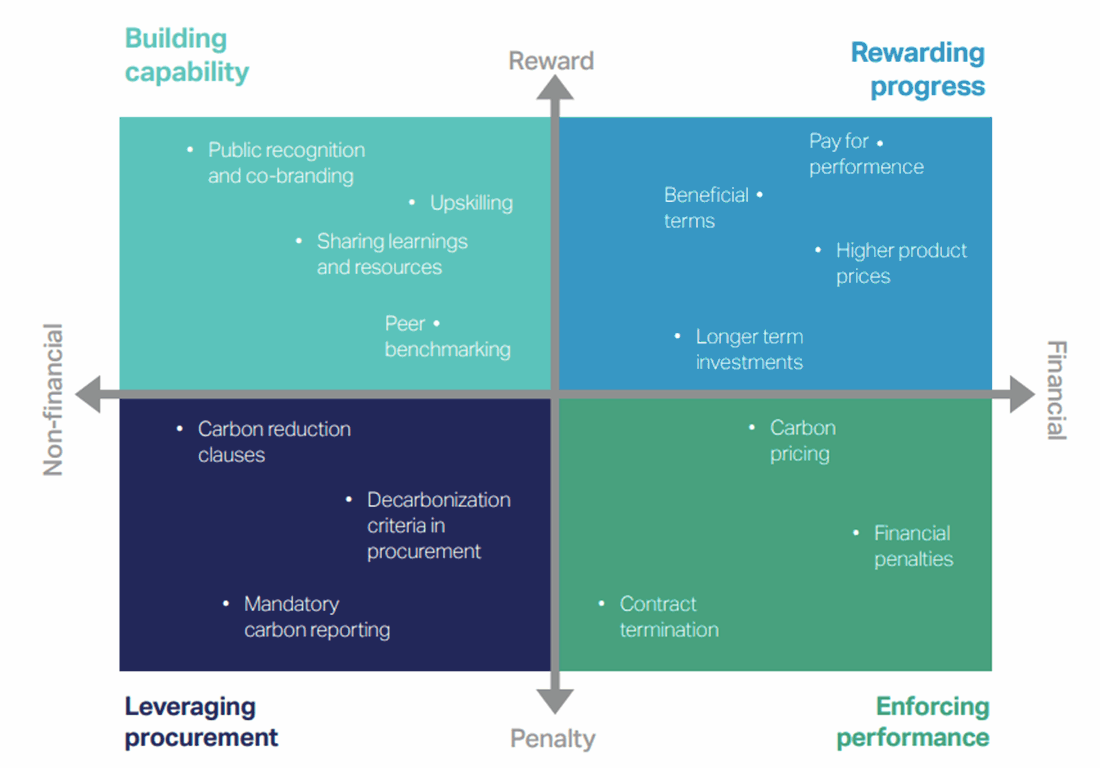

Ethical incentivization will be essential for the significant undertaking of compliance in such a tight timeframe. Below is a diagrammatic illustration of what this might look like:

Figure 2: Supply chain decarbonization incentivization framework ³

The WBSCD identifies 14 levers of implementation:

- Public recognition and co-branding

- Upskilling

- Sharing learnings and resources

- Peer benchmarking

- Longer term investments

- Beneficial terms

- Pay for performance

- Higher product prices

- Carbon reduction contract clauses

- Mandatory carbon reporting

- Decarbonization criteria in procurement

- Contract termination

- Carbon pricing

Having the right software to capture key data points, powered by executive leadership to drive user adoption are crucial to timely, accurate and compliant reporting.

Prof. David L Loseby MCIOB Chartered, FAPM, FCMI, FCIPS Chartered, MIoD, FRSA, MICW

References:

¹ IPCC, Summary for Policymakers (Table SPM.5: Characteristics of post-TAR stabilisation scenarios), in Climate Change 2007: Mitigation. Contribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change, ed. B. Metz, O.R. Davidson, P.R. Bosch, R. Dave, L.A. Meyer (Cambridge, United Kingdom and New York, NY, USA: Cambridge University Press, 2007).

² Technical Guidance for the Scope 3 emissions calculation: https://ghgprotocol.org/sites/default/files/standards/Scope3_Calculation_Guidance_0.pdf

Online course: https://ghgprotocol.org/scope3-standard-online-course

³ WBSCD: Incentives for scope 3 supply chain decarbonisation: accelerating implementation-November 2022